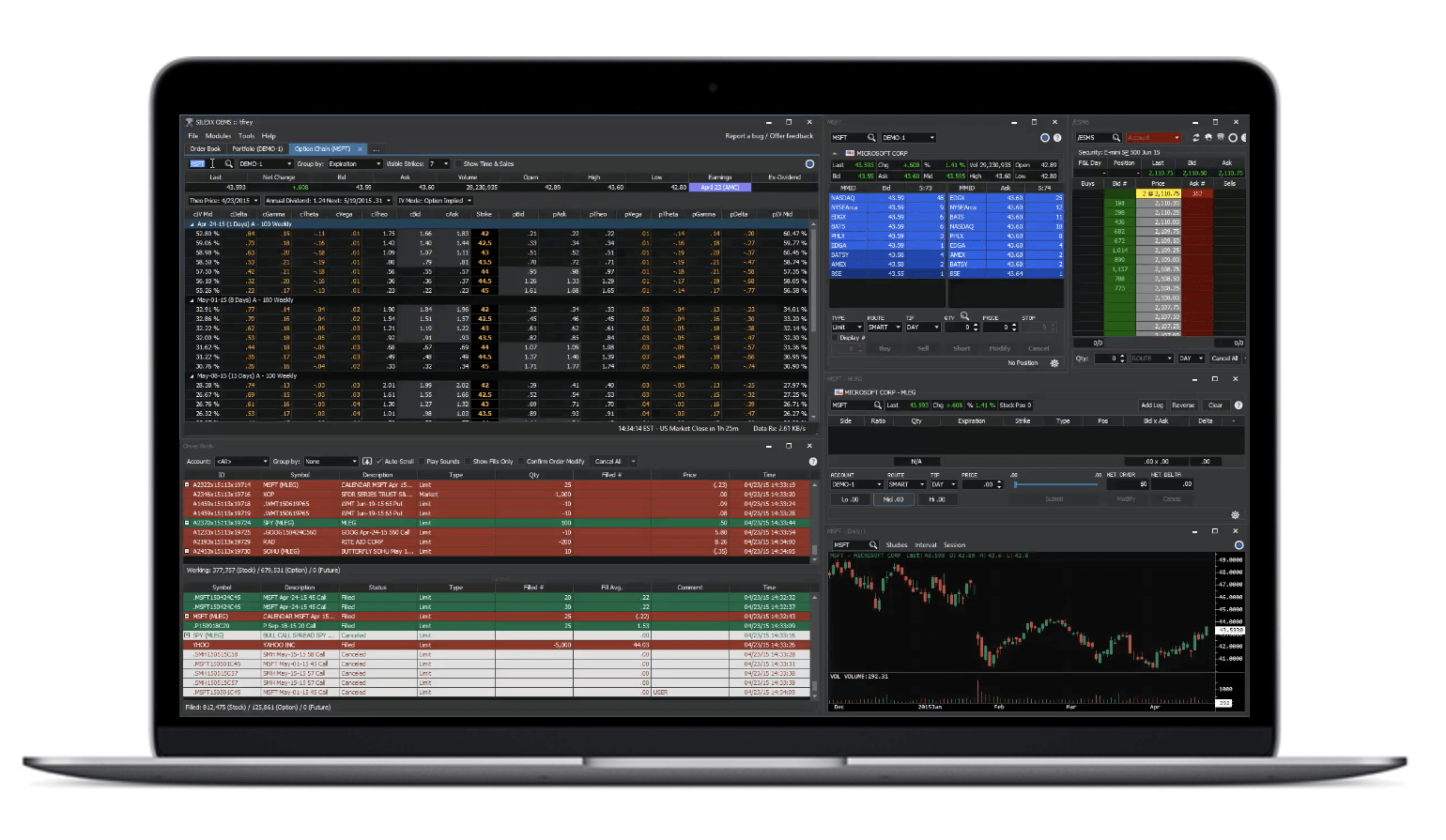

CBOE SILEXX, a multi -order execution system (OEM) that serves the professional market, announced a series of improvements in the context of version 25.9.

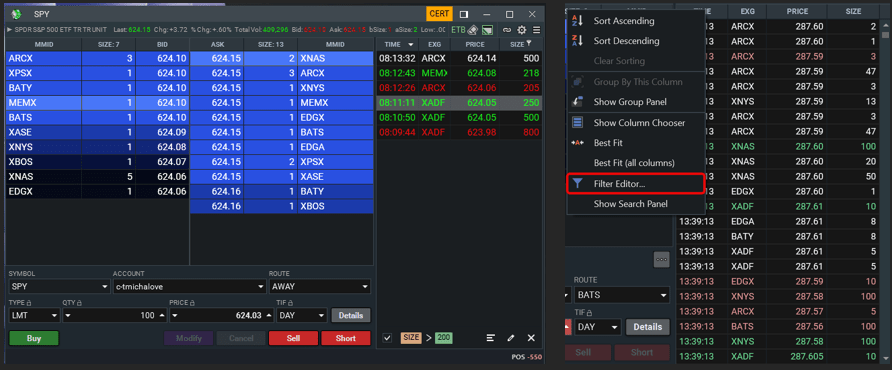

- Order ticket Filtering time and sales

Filters can be applied to time, exchange, price and size fields in the time and sales table. The filter processor can also access by right -clicking on a column header.

- Chain of Selection Export to Excel

An Excel Export button has been added to the options chain. This button click Action Records the enlarged expires in the chain of options and exports it to an Excel file. For example, if the first expiry is expanded to show the ATM+4 and the other shots collapse, the exit to Excel will display the first end with the ATM+4 visible, with the exception of collapses.

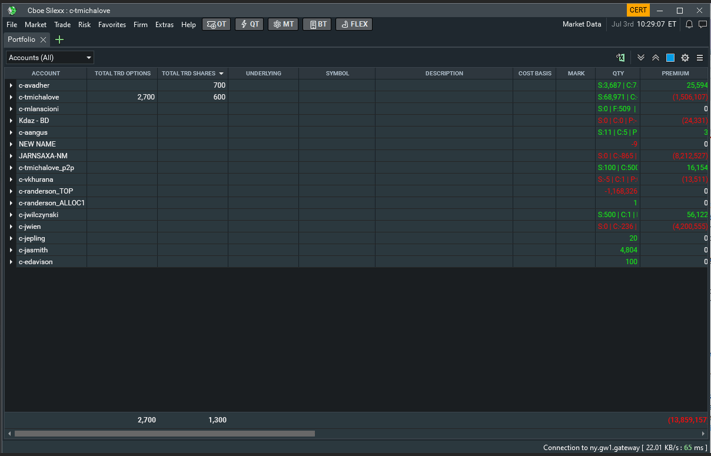

- Portfolio Total contracts and shares

Two new columns have been added to the portfolio unit, the total contracts that are negotiating and the total shares they negotiate. These two fields indicate the daily total volume of transactions, allowing traders and risk administrators to effectively monitor the overall activity in all accounts.

- Futures | The change of update, change % and PNL calculation methodology

Calculations for daily change, change rate and PNL day are now determined using the settlement price and not the previous one near alignment with industry standards.

- Order of Orders Support for Flex with the registered

The order importer now supports the introduction of Flex with the options listed. An up -to -date order sample standard is available in detail how to insert a mixture of flexible and reported legs.