The following is a version of Carolane De Palmas, a shopping analyzer at Retail FX and CFDS Broker Activetrades.

Tomorrow it brings two important catalysts for the forex market. Merchants will turn their attention to the FOMC minutes, which could shed light on the Fed trail to the expected interest rates in the coming months, before shifting the focus on Powell’s speech to Jackson Hole later this week. Prior to that, the foreground in the Asia-Pacific area will be in New Zealand’s Bank’s policy decision, where markets are placed for a possible interest rates. Together, these events could set the tone for coins purchases by remodeling interest rates on both sides of the Pacific, especially for forex pairs, including USD and NZD.

Reserve Bank of New-Zealand (RBNZ) is expected to reduce its basic interest rate to 3%

The New Zealand Reserve Bank (RBNZ) is at a critical juncture. At its meeting in July, the Central Bank decided to leave its main interest rate unchanged at 3.25%, stressing that increased uncertainty was pruded to expect more financial data on inflation, growth, as well as housing and labor markets.

RBNZ decided to wait before interest rates were cut, then they could evaluate if the domestic weakness became established, how inflation evolved and the way external developments – especially the impact of US invoices and the shift of the world – could be displaced.

But this period of patience seems to be over.

Market participants are widely awaiting that the Monetary Policy Committee will reduce OCR by 25 basis points to 3% during its meeting on Wednesday, August 20, continuing the relaxation cycle after the July cessation. According to a Bloomberg survey, 22 of the 23 economists expect a reduction in interest rates, which will bring borrowing costs to their lowest level in three years and will align politics with what is considered a widely neutral attitude.

A cut would provide some relief to the domestic economy, where the activity slows down the burden of weak demand, soft business investment and global trade pressures. The lower rates would help to facilitate economic conditions in supporting households and exporters, but also risk undermine the New Zealand dollar if markets interpret the traffic until the start of a deeper relaxation cycle. On the contrary, a closer perspective than RBNZ could lend the currency some durability, especially given the parallel uncertainty surrounding American monetary policy.

For traders, the basic focus will be not only the interest rate decision itself, but also the updated set of RBNZ views. In May, forecasts showed that the OCR is reduced to about 2.85% by the beginning of 2026, leaving the door open for further relaxation to just 2.75% if the conditions justify. Any signal that the central bank plans to accelerate or slow down this trajectory could cause significant volatility in NZD pairs.

The global environment has become an increasingly important factor for RBnz and recent commercial tensions with the United States stand out as a basic source of uncertainty. The central bank has already recognized that the highest US tariffs are likely to weigh the economy of New Zealand, weakening both growth and inflation. With the United States being the second largest export market in New Zealand, any reduction in demand for goods of goods could directly undermine export revenue, agricultural production and productive activity, and indirectly reshapes inflation expectations.

The bets increased after President Donald Trump announced a 15% invoice to New Zealand exports in early August, a measure that exceeded 10% initially marked. Politics was part of a broader US decision to impose higher invoices on countries that manage commercial surpluses and New Zealand was no exception.

In response, the Minister of Agriculture, Forests, Commerce and Investment Todd McClay announced a trip to Washington to participate in talks with US officials, stressing that the visit would be an opportunity to describe the cost of the new invoice and the cost of the new invoice. McClay emphasized the depth of the long -standing commercial corporate relationship between the two countries, noting that surpluses have been shifted over time and that total trade was generally complementary.

However, despite these assurances, the domestic economy is already feeling the executive. Production of production that has been involved in both May and June, the activity in the service sector has now declined for 17 consecutive months and unemployment increased to 5.2%, the highest level in five years. The housing markets, when a strong consumer wealth guide, have been stood by the recession from their pandemic. These developments emphasize the fragility of domestic demand and reinforce why external vibrations such as US invoices carry such a burden on shaping RBNZ perspectives.

Inflation, meanwhile, remains caught in a fine balance. He looked at 2.7% in the second quarter, reaching 2.5% in the March quarter. While inflation passes towards the top of the target zone 1 to 3% of RBNZ, policymakers continue to expect that inflation will gradually cool down, returning to about 2% at the beginning of 2026.

Dollar traders fueled with things for signs to shift policy

The liberation of Federal Reserve’s practices from its most recent meeting will be a critical time for traders this week, as markets are looking for confirmation that US interest rates cuts are back on the table. Investors are increasingly convinced that the Central Bank will reduce borrowing costs in September, with US money markets that are currently invoicing 93.5% for a 25 -point reduction, according to LSEG data. Proceedings could either enhance this belief or introduce doubts by defining the stage for increased volatility in dollars.

The July meeting itself was historic in itself. For the first time since 1993, many Fed rulers broke the ranks by the majority decision. Michelle Bowman and Christopher Waller openly favored a fourth point cut, underlining the growing internal debate over whether the Fed should move more aggressively to support a slowdown in the economy.

Recent data has leaning the balance towards relaxation. Most of the expected expectations of the labor market and inflation readings that have shown little evidence of prices -led prices have reduced concerns about cutting rates very soon. For markets, this reinforces the expectation that a September move is coming, with some policymakers and officials pushing even for a more bold step. Finance ministry secretary Scott Bessent has floated the idea of a 50 -base cut, while President Trump has repeatedly pressed Powell to avoid lower interest rates earlier this year, turning monetary policy into a politically charged arena.

If the minutes show widespread support for short -term relaxation, the dollar could be put under renewed pressure, as rhythm differences shift against it, especially against higher coins. On the other hand, if the document marks a hesitation among FOMC members or resistance to larger cuts, the market can reduce its expectations, giving the dollar some short -term support. Either way, the minutes will be a central guide to the FX market feeling in front of Powell’s speech at Jackson Hole later a week.

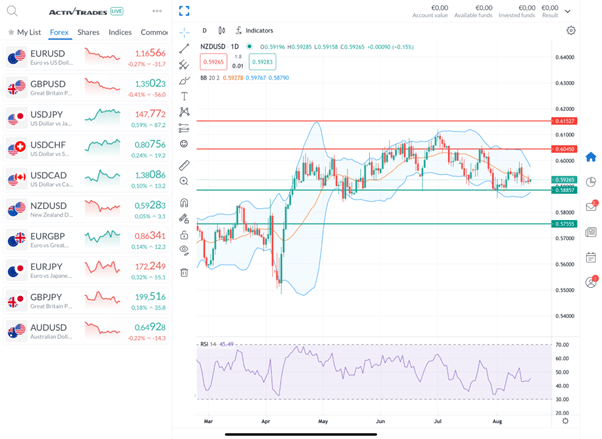

Technical Perspectives of the NZD/USD pair

Daily Nzd / USD Chart from the ACTIVTRADES online trading platform

Sources: RBNZ, The Wall Street Journal, Activtrades

The information provided does not constitute investment research. The material has not been prepared in accordance with the legal requirements aimed at promoting the independence of investment research and therefore must be regarded as marketing communication.

All information has been prepared by Activtrades (“AT”). The information does not contain a record of AT prices or an offer or attraction for a transaction in any financial instrument. No representation or guarantee of the accuracy or completeness of this information is given.

Any material provided does not take into account the specific investment target and the financial situation of any person who may receive it. The previous performance is not a reliable indicator of future performance. AT provides a service only for execution. Consequently, every person acting for the information provided does so at his own responsibility. Forecasts are not guarantees. Prices can change. The political risk is unpredictable. The actions of the Central Bank may vary. Platform tools do not guarantee success.