The following is a version of Carolane De Palmas, a shopping analyzer at Retail FX and CFDS Broker Activetrades.

After amazing purchases last month holding the cash rate of 3.85%, the Australian bank is now under renewed pressure for action. The second quarter data has painted a mixed image inflation, relaxing faster than expected, but economic growth has stopped and the early signs of labor market weakness emerge. This combination feeds on the expectations that the RBA will reduce the rates by 25 basis points to 3.60% during August’s meeting, continuing its cautious axis from the tightening cycle.

Markets have already been invoiced in this move, along with another cut before the end of the year, marking a steady reversal of 4.35%-a 12-year high reached the fight against unexpectedly powerful inflation. The question now is whether the RBA will move quickly to support the economy or maintain a measured rate amid global monetary uncertainty.

RBA has been set to reduce rates as inflation is cooled and growth drifts

Australia’s inflation pulse has slowed abruptly in the June quarter, providing a weaker rise in consumer prices over four years and giving the Australian reserve bank a very necessary suspension in its struggle against the pressures of transmitic prices. Inflation of the core-a measure that is closely monitored by policymakers-broke into a new three-year low, with the decorated average increasing only 0.6% compared to the quarter and 2.7% during the year. This is reduced from 2.9% in March and sits comfortably near the middle of the RBA target range of 2-3%.

Soft reading is a surprise to many on the RBA board, which had stopped the interest rate cycle in July from concern that basic inflation could prove stubborn. While housing, food and health care costs continued to increase, the decline in transport prices contributed to the overall increase. Temporary government discounts on electricity and children’s care also played a role, promoting the growth of the CPI with a title of 0.8% for the quarter and 2.1% per year – the lowest of the early 2020s, but with the RBAs, the RBA expects it to be 3% before the RBA.

For Governor Michelle Bullock, these latest data confirm that the RBA has the space to “reduce” the reduction of monetary restriction, as westpac’s economists have put it. Markets are now betting on a 25 -base interest rate reduction in August, with more reductions probably in November, February and May of the following year.

The case of relaxation exceeds inflation. Economic growth was sluggish, with GDP growing only 0.2% in the first quarter-the rate expected by economists-and holds a sluggish of 1.3% annually. This persistent sluggishness is in danger of consolidating the weak costs of households, as uncertainty urges Australians to save rather than spend.

The labor market, while still historically tight, also loses some steam. June saw a meager 2,000 job increase, well below the prediction of 20,000, while unemployment was up to 4.3% from 4.1%. Employment growth is expected to decline to 1.0% by the end of the year, even when KPMG predicts that the unemployment rate will remain at 4.3%-a level that continues to support household resilience, but does nothing to produce new inflationary pressure.

In the short term, the lower rates could provide much support for both the economy and the labor market, preventing further deterioration. However, economists point out that monetary policy will not be enough. Without long -term reforms that enhance productivity, Australia is in danger of slipping into a model of slow growth and lukewarm job creation, even if inflation remains.

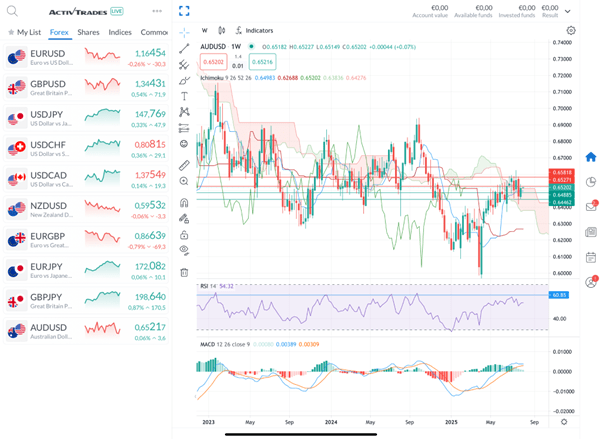

AUD/USD Weekly Technical Perspective – Before RBA decision

Weekly AUD/USD diagram from Activtrades

By the end of 2024, the wider trend has been shifted from a steep downward trend in a gradual phase of recovery. However, the race was unstable, reflecting the trailer between interest rates and global danger. Recent integration around 0.6500 shows that the market is waiting for a catalyst – probably the RBA meeting – to determine the next direction.

Price action remains close to the Ichimoku weekly cloud limit, indicating that the market is central. The fact that the couple entered the cloud earlier in Q2, but failed to break decisively above, suggests constant uncertainty. A prolonged movement above 0.6520 – the top of the cloud – would be a suspensive signal, opening the door to the 0.6700 zone. On the contrary, a rejection here could send the couple back to 0.6445 and possibly 0.6400, where recent support was formed.

RSI (14) hovers near 54, which shows a neutral momentum – either over -corruption or hyperprostarcement – which gives room for movement in any direction, possibly depending on the RBA result. The MacD index remains in positive territory with light bias, but the rods are talked about, indicating the decline in the rise in front of the announcement.

Basic levels for monitoring:

- Resistance: 0.6527 (Kijun-Sen), 0.6580 (Cloud Top), 0.6700 (May High)

- Support: 0.6488 (recent Swing Low), 0.6445 (Tenkan-Sen), 0.6400 (June Low)

Threshold

By cooling inflation faster than expected, growth growth and labor market that shows early signs of stem, the RBA is on track for another interest rate cut – a fact that could shape the next move on AUD/USD. The couple, now close to 0.6520, hover over a cluster of basic supports, but remain covered by resistance by Ichimoku Cloud and previous swing highs.

Technically, AUD/USD is in a central juncture. The weekly diagram shows the price test the upper limit of integration range and Ichimoku Cloud, with the RBA decision setting the direction. A unblocking over 0.6580 or one drop below 0.6445 could adjust the tone for the next major trend.

Sources: KPMG, Australian Statistics Office, CNBC, Reuters, Ing, Activtrades

The information provided does not constitute investment research. The material has not been prepared in accordance with the legal requirements aimed at promoting the independence of investment research and therefore must be regarded as marketing communication.

All information has been prepared by Activtrades (“AT”). The information does not contain a record of AT prices or an offer or attraction for a transaction in any financial instrument. No representation or guarantee of the accuracy or completeness of this information is given.

Any material provided does not take into account the specific investment target and the financial situation of any person who may receive it. The previous performance is not a reliable indicator of future performance. AT provides a service only for execution. Consequently, every person acting for the information provided does so at his own responsibility. Forecasts are not guarantees. Prices can change. The political risk is unpredictable. The actions of the Central Bank may vary. Platform tools do not guarantee success.