Hard to believe we’ve already closed the books for the first half of 2024 – and what a six months it’s been!

We at FNG have seen record traffic and visitor numbers month after month (more on that below), and it’s no wonder, given the interesting stories and topics that have helped reshape the FX and CFD trading industry in ways no one else could. to predict six months ago.

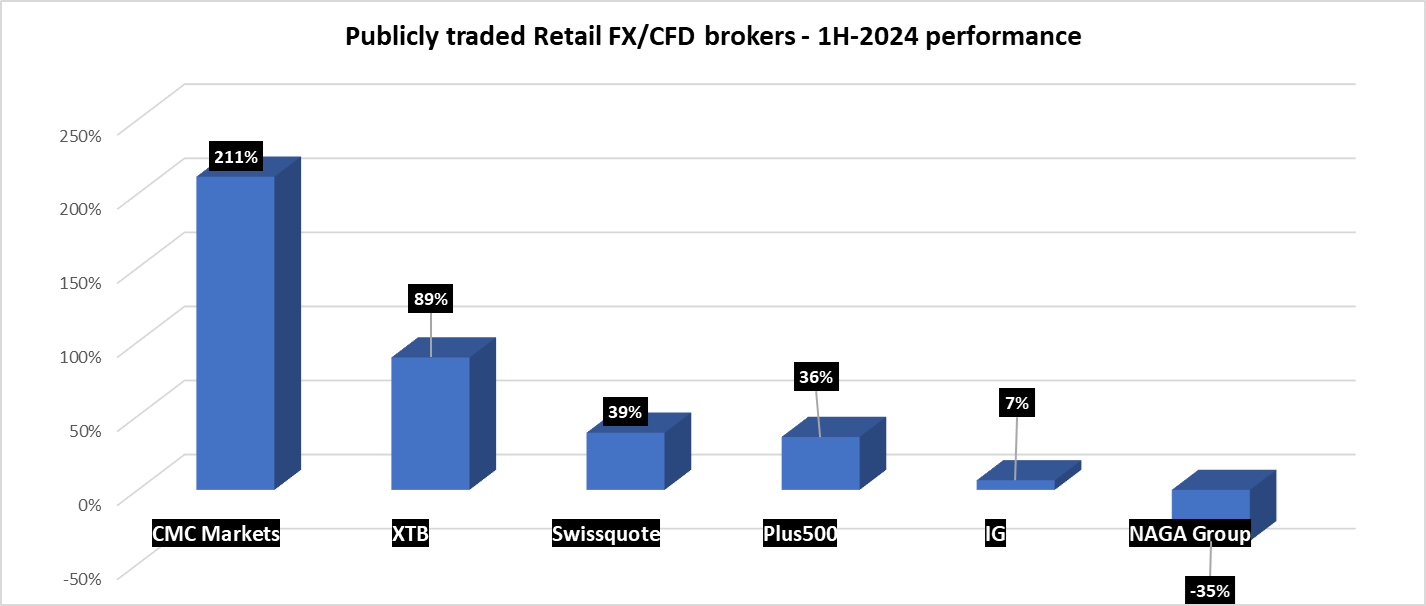

Also indicative of the change is the fairly impressive performance of the stock market traders, who saw a collective 50%+ increase in the share price in the first half of the year, some setting all-time highs.

Before we get to the top stories and topics of 1H 2024 in Forex and CFDs, we at FNG would like to take this opportunity to thank our readers for making FNG the clear #1 most trusted and popular news site in the field. Almost every big story was reported first or exclusively on FNG, and it showed in our record month-on-month visitors, which are more than 2x what they were at this stage last year.

Before we get to the top stories and topics of 1H 2024 in Forex and CFDs, we at FNG would like to take this opportunity to thank our readers for making FNG the clear #1 most trusted and popular news site in the field. Almost every big story was reported first or exclusively on FNG, and it showed in our record month-on-month visitors, which are more than 2x what they were at this stage last year.

And now, to this year’s (so far) top stories and topics…

1. Stock traders see a 58% rise in the stock price.

Since we already mentioned it in our introduction above, we’ll take it first. Led by CMC Markets which more than tripled its share price after a disappointing 2023 and Switzerland’s Swissquote and Poland’s XTB entering 2H 2024 with their share prices at or near all-time highs, traders they have left their shareholders quite happy so far. year.

We note that this performance occurred against the backdrop of fairly low volatility in the forex markets, with the EURUSD benchmark trading in a fairly tight 1.07-1.09 band for most of the past few months. But even so, brokers put up pretty good numbers as healthy equity markets brought more retail traders to the table and as brokers also focused on cost-cutting measures so more revenue fell into the bottom line.

| Share price from… | Mkt Cap | |||

| 31-Dec-23 | 30-Jun-24 | % change | (USD $M) | |

| CMC Markets | 105 | 327 | 211% | 1135 |

| XTB | 37.82 | 71.64 | 89% | 2102 |

| Swissquote | 204.6 | 283.6 | 39% | 4806 |

| Plus500 | 1669 | 2266 | 36% | 2176 |

| IG | 769 | 819 | 7% | 3872 |

| NAGA Group | 1.07 | 0.7 | -35% | 40 |

| Average performance | 57.9% | |||

| Average performance | 37.2% | |||

2. Support the chaos of the company’s trading platform.

Retail commodity trading, also referred to as funded investor firms, have been around for a long time and have essentially acted as brokers to numerous retail FX and CFD brokers who execute trades initiated by support firm clients.

Not really a big deal – until earlier this year, when MT4 and MT5 developer MetaQuotes decided to cut off all traffic from propaganda companies, given the companies’ tendency to take on what MetaQuotes considers clients they really shouldn’t, such as traders US based retailer.

A number of propaganda firms were summarily axed after brokers received ultimatums from MetaQuotes to either cease operations or risk losing their MT4 and MT5 licenses.

A number of propaganda firms were summarily axed after brokers received ultimatums from MetaQuotes to either cease operations or risk losing their MT4 and MT5 licenses.

What followed was nothing but a mad rush by both brokers and support companies to add MT4/MT5 alternative trading platforms, most notably Devexperts’ DXtrade, Match-Trade’s Match Trader, Spotware’s cTrader and SiRiX by Leverage. Brokers who had decided to add “backup” platforms to MT4 and MT5 suddenly saw the exercise as not just insurance in case of a problem with MetaQuotes (like when MT4 and MT5 were temporarily removed from the Apple App Store in late 2022), but as good business practice, and necessary if they wanted to work with the support companies.

3. Failure of neo-mediators.

The last few years have seen the rise of a new type of online broker, especially in the EU – the neo-broker. Mainly looking for younger clients who do things on their mobile device, several of these brokers have emerged trying to be ‘the Robinhood of Europe’ offering a mix of leveraged trading (FX, CFDs) as well as ‘traditional’ stock and index trading and basic banking services.

The last few years have seen the rise of a new type of online broker, especially in the EU – the neo-broker. Mainly looking for younger clients who do things on their mobile device, several of these brokers have emerged trying to be ‘the Robinhood of Europe’ offering a mix of leveraged trading (FX, CFDs) as well as ‘traditional’ stock and index trading and basic banking services.

It sounded good on paper, but obviously harder to execute in the real world, as two of the more familiar names – BUX and FlowBank – are basically gone. Amsterdam-based BUX was effectively bought out by one of its original backers, ABN Amro, late last year after a failed UK launch, a failed launch of the CFD brand (Stryk, outside Cyprus) and ongoing losses.

And at the end of the 1st half of 2024, Geneva-based FlowBank was forced into bankruptcy by the Swiss regulator FINMA, which claimed that FlowBank had mounting debt and insufficient capital levels to operate. FlowBank’s situation has also hit London-based LCG, one of the oldest names in the FX and CFD brokerage business, which is now stuck in the unpleasant position of being a subsidiary of a now bankrupt company.

4. Management moves around a lot – including CEOs.

One of the constants in the FX and CFD business is change. And that theme has been true when considering the numerous top management moves we’ve seen over the past six months in the industry, including several at the top rung of the ladder, in the CEO’s office.

One of the constants in the FX and CFD business is change. And that theme has been true when considering the numerous top management moves we’ve seen over the past six months in the industry, including several at the top rung of the ladder, in the CEO’s office.

Most notable among the C-Suite changes was Estonia-based online broker Admirals, which saw the departure of longtime CEO Sergei Bogatenkov and nearly its entire board after Admirals saw its revenue collapse 41% in 2023. Company founder Alexander Tsikhilov has assumed the role of CEO for the time being at Admirals.

Also of note is the CEO change at NAGA Group, with Capex.com CEO and shareholder Octavian Patrascu taking the reins of NAGA ahead of Capex.com’s acquisition of NAGA, which is expected to close in early 2 semester of 2024.

Other notable CEO-level moves reported at FNG in the past six months include;

5. Continued industry consolidation.

As the forex and CFD industry continues to not only prosper but mature, we continue to see a number of broker acquisitions. In addition to the Capex.com-NAGA Group deal announced late last year, which we noted above, some of the other interesting M&A activity and news in the sector over the past six months include:

As the forex and CFD industry continues to not only prosper but mature, we continue to see a number of broker acquisitions. In addition to the Capex.com-NAGA Group deal announced late last year, which we noted above, some of the other interesting M&A activity and news in the sector over the past six months include:

- Exclusive: HYCM control was sold through a management buyout.

- Saxo Bank is hiring investment bankers to explore the sale.

- Hargreaves Lansdown’s board agrees to a £5.4bn takeover of the firm after earlier rejecting a lower offer from private equity buyers CVC, Nordic Capital and the Abu Dhabi Investment Authority.

What does the second half of 2024 hold for FX and CFDs brokers, platform and technology providers, liquidity providers and the wider trading community? Stay tuned to FNG!